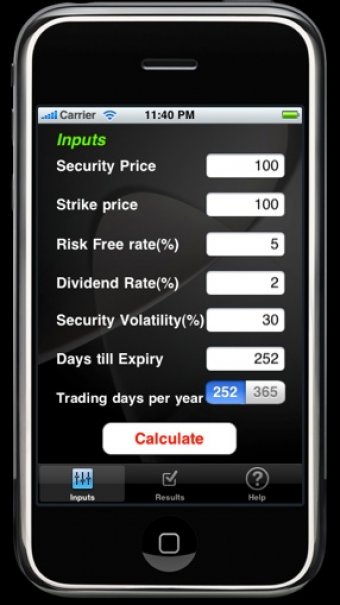

iOptions is a unique application that computes European option prices and Greeks (Delta, Gamma, Rho, Theta and Vega) using Black-Scholes model.

It takes as input the current Security Price, the Strike Price, the annualized risk-free rate, the annualized Dividend Yield, the annualized Volatility of the security and the number of days till expiry of the option.

It also gives a good approximation of the American put price using Cox, Ross and Rubinstein binomial tree model with Broadie and Detemple adjustment.

In addition, it can price Futures (Black-Scholes model) and currencies (Garman-Kohlhagen model) with adjustment to the dividend yield in inputs.

Comments